In the fast-paced world we live in today, it often seems as though we are just going through the motions. We tick off items from an endless to-do list. If we stop and think, we see that each day gives us a new opportunity. We can grow. We have the opportunity to gain knowledge. Additionally, we can contribute positively to our environment. This blog will explore the importance of seizing daily opportunities. It will discuss the necessity of aligning our actions with our core values. You will find actionable strategies for fostering a growth-focused and positive mindset.

A . EMBRACING DAILY POSSIBILITIES

A.1 The Power of a New Day

Every day is a new opportunity, a clean slate brimming with limitless potential. The sun comes up, illuminating the fresh possibilities that lie ahead. This idea is more than just artistic; it serves as a strong reminder that our daily decisions shape our lives. The arrival of a new day signifies optimism, rejuvenation, and the possibility for transformation.

Think about the tale of Thomas Edison, who is well-known for stating, “I have not failed.” “I’ve discovered 10,000 ways that don’t succeed.” His unwavering commitment to innovation shows that every day presents a chance to reboot. We can learn from our mistakes and aim for excellence. When we welcome the opportunities of a new day, we can engage in learning experiences. These experiences can foster personal growth. They can also promote professional development.

A.2 The Ripple Effect of Small Actions

The potential for positive impact starts with small actions. Every interaction we have, no matter how minor it seems, can create a ripple effect that influences others. Smiling at a stranger can brighten someone’s day. Offering a helping hand or sharing words of encouragement can inspire them to pay it ahead.

Consider the example of a small act of kindness that resulted in a significant transformation. In a busy coffee shop, one customer covered the cost of the coffee for the individual behind them in line. This gesture of kindness initiated a ripple effect, where each person in line bought the order for the next customer. What started as a simple act evolved into a day-long movement of compassion. This shows that by welcoming daily opportunities, we can foster a culture of kindness and positivism.

A.3 Growth Through Challenges

Life is full of challenges. Often, we discover our greatest chances for personal development when we face adversity. When encountering difficulties, we can either allow frustration to overwhelm us or see these challenges as opportunities for personal growth. Welcoming the idea of growth involves altering how we view challenges.

Think about the tale of J.K. Rowling encountered many rejections before successfully publishing the Harry Potter series. Her path was filled with difficulties, including personal battles and financial difficulties. Nonetheless, she decided to see these challenges as chances to enhance her writing skills and bolster her determination. Today, Rowling is among the most accomplished authors in history. This highlights the importance of viewing challenges as opportunities for personal development.

B. THE IMPORTANCE OF LEARNING

B.1 Lifelong Learning as a Value

A crucial element of personal development is dedicating oneself to continuous learning. In a fast-evolving world, the capacity to adjust and gain new insights is extremely valuable. Adopting the perspective of a lifelong learner involves understanding that learning goes beyond traditional education. It includes experiences. It also encompasses connections with others, and personal introspection.

Albert Einstein famously stated that “intellectual development should start at birth and continue until death.” This viewpoint motivates us to pursue knowledge in all areas of our lives. We have endless chances to learn each day. We can read books. We can join in workshops. We can have impactful discussions or just watch the world around us.

B.2 Learning from Others

We can gain a great deal from the experiences and perspectives of other people. Engaging with a variety of viewpoints enhances our comprehension of the world and promotes empathy. Interacting with people from diverse backgrounds and cultures helps us expand our perspectives and rethink our preconceived notions.

Think about the influence of mentorship. A mentor can offer direction, impart important knowledge, and motivate us to exceed our boundaries. We can avoid frequent mistakes by gaining insights from those who have taken similar journeys. This also speeds up our development. Learning from others broadens our understanding. It also strengthens our relationships with the people in our lives.

B.3 Embracing Mistakes as Learning Opportunities

Errors are an unavoidable aspect of life, yet they are often perceived in a negative light. Rather than avoiding failure, we ought to view it as a precious chance for growth and learning. Every mistake holds a lesson that can influence our future choices and behavior.

Think about the tale of a budding entrepreneur who started a new business. After encountering various difficulties, like financial losses and operational issues, they decided to thoroughly evaluate each error. By recognizing their mistakes and modifying their approach, they ultimately succeeded in creating a successful business. This experience emphasizes the value of viewing failure as a pathway to success.

C. ALIGNING ACTIONS WITH VALUES

C.1 DEFINING PERSONAL VALUES

To create a positive difference in the world, it’s crucial to ensure our actions reflect our fundamental values. Values are the fundamental principles that influence our beliefs, choices, and actions. They act as a guiding principle, helping us navigate our lives.

Take a moment to consider what matters most to you. Is it principles like integrity, kindness, creativity, or a commitment to social justice? Identifying your core values can provide clarity on your purpose and motivate you to pursue impactful actions. When our behaviors align with our values, we feel a sense of satisfaction and genuine self-expression.

C.2 Living Authentically

Living authentically involves staying true to who you are and your principles, despite external societal pressures. It takes bravery to uphold your convictions and make decisions that reflect your values. By living true to ourselves, we motivate others to embrace authenticity, generating a wave of positive transformation.

Take the case of Malala Yousafzai, who advocated for girls’ education despite facing significant challenges. Her steadfast dedication to her principles and her readiness to advocate against injustice have motivated millions globally. By being true to herself, she has significantly influenced the lives of many young girls.

C.3 The Role of Gratitude

As we strive to create a positive influence, fostering an attitude of gratitude is vital. Gratitude redirects our attention from what we don’t possess to what we do have, cultivating a mentality of abundance. When we greet each day with gratitude, we increase our awareness of opportunities. These opportunities for personal growth and learning are all around us.

There are various ways to cultivate gratitude. You can maintain a gratitude journal. You can also show appreciation to the people in our lives. When we recognize the positive facets of our lives, we enhance our perspective. This recognition enables us to engage in actions that reflect our values.

D. PRACTICAL WAYS TO EMBRACE GROWTH AND POSITIVITY

D.1 Setting Daily Intentions

A great way to welcome the opportunities of each day is by establishing daily intentions. Intentions serve as a framework for our behavior, keeping us concentrated on what is genuinely important. Every morning, spend some time reflecting on your goals. Consider the kind of presence you want to cultivate in the world.

For instance, you could aim to cultivate kindness, embrace new experiences, or focus on self-care. By intentionally establishing your goals, you create a guide for your day. This enables you to make decisions that reflect your values.

D.2 Engaging in Mindfulness

Mindfulness techniques help us remain present. They include meditation and deep breathing. These practices develop an awareness of our thoughts and emotions. Integrating mindfulness into our everyday life can improve our capacity to respond thoughtfully to both challenges and opportunities.

Think about spending a few minutes daily practicing mindfulness meditation. This practice can help you develop a sense of tranquility, clarity, and concentration. It allows you to start each day with intention and direction.

D.3 Taking Action, No Matter How Small

Making a positive impact doesn’t always necessitate significant actions. Consistent small actions can result in substantial change. You can help out in your community. You can support local businesses. You can check in on a friend who needs help. Every effort matters.

Start by pinpointing a simple daily action you can take to create a positive effect. This can be as straightforward as writing a thank-you note, praising a coworker, or cleaning up trash in your community. By engaging in small acts of kindness, you foster a positive environment and encourage others to follow your example.

D.4 Surrounding Yourself with Positivity

The individuals we associate with shape our thoughts and behaviors. To foster a positive and growth-driven atmosphere, surround yourself with people who motivate and encourage you. Participate in discussions that promote growth and knowledge acquisition.

Think about becoming a member of community groups, clubs, or online forums that reflect your interests and values. Being around people who share your mindset builds a support system that encourages motivation and responsibility.

D.5 Continuous Reflection and Adaptation

As we develop and gain knowledge, it’s important to consistently reflect on our experiences. Consistently evaluate your actions, beliefs, and objectives to confirm they are still in alignment. Reflection enables us to modify our strategies and make essential changes as we face the difficulties of life.

Think about dedicating some time every week for introspection. Consider reflecting on questions like: What new insights did I gain this week? In what ways did my behavior align with my principles? What changes can I implement in the future? Engaging in this practice not only boosts your self-awareness but also enables you to make more deliberate decisions.

CONCLUSION

Each day presents a fresh chance to develop, acquire knowledge, and positively influence our surroundings. When we embrace the opportunities that each day offers, we change our own lives significantly. We also change the lives of those around us. When we align our actions with our values, we can live genuinely and motivate others in our vicinity.

As we journey through the intricacies of life, let us keep in mind the significance of minor actions. We should recognize the value of continuous learning. We must also remember the influence of uplifting connections. By working together, we can foster an environment of growth, kindness, and positivity that extends well beyond our personal experiences.

Each morning as you rise, pause for a moment to appreciate the possibilities that the day may bring. Establish your goals, practice mindfulness, and keep in mind that every action matters. You can create impact in your own life. You can also affect the lives of those around you. Seize the opportunities. Ensure your actions align with your values. Observe how you foster a ripple effect of positive transformation in the lives around you.

Today, I want to take a moment to put some light on the extraordinary legacy of Eleanor Roosevelt, a pioneering figure in American history who moved beyond her position as First Lady to emerge as a powerful champion for human rights, social justice, and the empowerment of women. Her profound statement, “The future is owned by those who have faith in the beauty of their dreams,” serves as a compelling reminder of how our aspirations influence both our lives and the world around us. By delving into the deeper implications of this quote, we will reveal the importance of cultivating our ambitions and how our steadfast faith in these dreams can guide us toward a more promising and just future for everyone. Come along with me as we set out on this uplifting adventure together.

INTERPRETATION

The statement highlights two essential elements: faith and aesthetics. Believing in your dreams means having confidence in the potential for a brighter future. It indicates that dreams are more than just fanciful thoughts; they are significant insights that can motivate action and transformation. The word “beauty” in this context suggests that our aspirations should be based on optimism, imagination, and a sense of hope. Beauty in dreams can take many shapes, whether it’s through individual aspirations, shifts in society, or even worldwide changes.

Embracing the beauty of our dreams also involves acknowledging their importance. It inspires us to look past the ordinary and the present moment, prompting us to recognize the possibility of greatness found in our ambitions. This conviction is crucial, as it acts as the driving force behind action and persistence. Without faith, dreams can quickly turn into nothing more than fleeting wishes—ideas that slip away without being acted upon.

THE IMPORTANCE OF NURTURING DREAMS

1. Personal Growth and Development

Fostering our aspirations is crucial for individual development. Dreams frequently mirror our innermost wishes, beliefs, and interests. By dedicating ourselves to recognizing and nurturing these goals, we set off on a path of self-exploration. We gain deeper insights into ourselves—our genuine desires, our motivations, and our potential accomplishments. This journey of exploration enhances our self-awareness and promotes resilience and adaptability.

2. Fostering Creativity and Innovation

Dreams frequently serve as a source of inspiration and originality. By permitting ourselves to dream big, we expand our minds to embrace new opportunities and concepts. This imaginative process can result in innovative solutions and progress in fields such as the arts, sciences, technology, or social activism. History is filled with instances of people and groups who had the courage to dream, ultimately altering the trajectory of human events. From innovators such as Thomas Edison to creators like Vincent van Gogh, the brilliance of their visions has made a lasting impact on the world.

3. Building a Supportive Community

By openly expressing our dreams to others, we foster a feeling of community and encouragement. Individuals are frequently motivated by the ambitions of their peers. This shared enthusiasm can foster a supportive atmosphere where aspirations are both recognized and promoted. When people collaborate towards shared objectives, they can enhance their influence. Social change movements typically start with a collective aspiration for a better world, bringing together diverse people who share a unified vision.

4. **Resilience in the Face of Adversity**

Life is filled with difficulties and hurdles, and our aspirations may face trials due to hardships. Nonetheless, having faith in the beauty of our aspirations can offer the motivation required to keep going. During challenging times, our dreams serve as a source of purpose and inspiration, encouraging us to continue pushing ahead. This resilience is essential for overcoming challenges and attaining success. Numerous successful people have encountered substantial obstacles, but their steadfast faith in their aspirations motivated them to persist in pursuing their objectives.

THE ROLE OF ACTION IN REALIZING DREAMS

Although having faith in dreams is essential, it’s just as important to understand that dreams by themselves won’t bring about success. Action serves as the link that transforms our dreams into reality. This entails establishing clear goals, developing practical plans, and consistently striving to achieve those aims.

1. **Setting Goals**

In order to cultivate our dreams successfully, we need to transform them into attainable objectives. This process entails dividing our broader goals into smaller, achievable tasks. Establishing SMART (Specific, Measurable, Achievable, Relevant, Time-bound) goals can clarify our direction and offer a framework for advancement. Goals act as checkpoints that help maintain our focus and motivation as we strive toward our overarching vision.

2. **Cultivating a Growth Mindset**

Embracing a growth mindset is essential for achieving our aspirations. This perspective helps us see challenges as chances for learning and development instead of as impossible hurdles. When we pursue our dreams with a growth mindset, we become more receptive to feedback, more inclined to embrace risks, and better equipped to bounce back from challenges. Accepting failures as a natural aspect of the journey provides us with important insights that can improve our future endeavors.

3. **Building a Support System**

Having supportive people around us who share our belief in our dreams can greatly influence our journey. This support network may consist of friends, family members, mentors, and coworkers—individuals who motivate us, offer advice, and keep us responsible. These connections can be extremely beneficial, providing fresh viewpoints and insights that can assist in sharpening our objectives and approaches.

4. **Celebrating Progress** As we pursue our aspirations, it’s important to acknowledge and celebrate our progress, regardless of its size. Recognizing our successes cultivates a feeling of achievement and strengthens our faith in the value of our aspirations. Recognizing milestones throughout our journey can inspire us to keep chasing our goals, as it highlights the progress we’ve achieved and the possibilities that await us.

THE RIPPLE EFFECT OF ASPIRATIONS

When people have faith in the beauty of their dreams and actively pursue them, the effects can reach far beyond their own lives. The pursuit of dreams can create a ripple effect that impacts families, communities, and even worldwide movements.

1. **Inspiring Others**

When we chase our dreams with enthusiasm and resolve, we motivate others in our circle to follow suit. Our actions can inspire hope, encouraging others to have faith in their own dreams. This shared motivation can foster a culture of ambition and innovation, where people encourage and elevate each other in their endeavors.

2. **Social Change and Progress**

Numerous major progressions in society arise from the aspirations of those who had the courage to imagine a better future. Leaders in civil rights, environmental advocates, and innovators across different sectors have all been instrumental in shaping the future. Their faith in the power of their dreams has driven impactful changes that not only enhance their own lives but also positively affect many others. By cultivating our aspirations, we play a role in creating a legacy of advancement and constructive transformation.

3. **Contributing to a Shared Vision**

When aspirations come together with a common vision for the future, they can foster significant movements. Shared goals can bring together different groups, promoting teamwork and collaboration. For instance, the movements advocating for climate justice, social equity, and gender equality all arise from a common aspiration for an improved world. By embracing the vision of these dreams, people can unite to tackle urgent global issues and strive for sustainable solutions.

CONCLUSION

Eleanor Roosevelt’s statement, “The future belongs to those who believe in the beauty of their dreams,” highlights the enduring significance of dreams and the necessity of fostering them. Having faith in our dreams, along with purposeful efforts, can foster personal development, innovation, adaptability, and societal transformation. As we journey through life’s challenges, let us stay committed to our dreams, nurture them thoughtfully, and encourage others to pursue theirs as well. By embracing the allure of our dreams, we can create a better future—not just for ourselves, but for future generations as well. Chasing our dreams isn’t always a simple task, but it is certainly among the most fulfilling experiences we can embark on. Cherish your aspirations, have faith in their significance, and take the actions needed to bring them to life. The future belongs to those who have the courage to dream.

A taxable supply is a commonly used expression in relation to Value Added Tax (VAT) systems. It pertains to any exchange of goods or services for an agreed payment (typically money) by a legally recognized company with the intention of generating a financial gain. Put simply, it is a purchase or sale that is liable for value-added tax (VAT).

In a value-added tax (VAT) system, the tax is applied at every step of the supply process, including the manufacturer, the retailer, and the final consumer. This guarantees that the final cost of the tax falls on the consumer, but it also implies that businesses must collect and pay the tax to the government as representatives of the tax authorities.

To be classified as taxable, a supply must satisfy specified criteria established by the tax authorities. These standards might differ across different regions, but typically they encompass the following factors:

The supply must be made by a taxable person – To be eligible for taxation, the supply must be conducted by an individual who is officially registered for VAT. This implies that the individual or organization providing the goods or services needs to be involved in economic activities consistently and must have surpassed the VAT registration limit established by the tax authorities.

The supply must be made in the course of business – The taxable person must make the supply as part of their business activities. This indicates that it needs to be done in relation to someone’s economic pursuits and should be done regularly with the aim of generating income.

The supply must be made for consideration – The provision needs to be given in return for something, typically payment. This implies that there should be a given monetary worth assigned to the items or services being traded, and that worth must be paid by the person receiving the supply.

The supply must be made in the jurisdiction where VAT is applicable – The provision needs to occur in a region where Value Added Tax (VAT) is enforceable. This indicates that the supply needs to be conducted in a country or area where there is an existing VAT system, and the tax must be imposed at the correct rate.

The supply must be a ‘taxable supply’ as defined by the tax authorities – In conclusion, for the supply to be subjected to taxes, it is necessary that it fulfills the specific requirements determined by the tax authorities. This could involve specific items or cases that are not included or exempt, and regulations about when and how the tax is computed.

In reality, taxable supplies can cover various transactions, such as selling goods, offering services, and importing goods from different nations. Some typical instances of supplies that are subject to taxation comprise:

– The sale of goods in a retail store

– The provision of professional services, such as legal or accounting services

– The rental of commercial property

– The importation of goods from overseas

It should be emphasized that not all supplies are subject to taxation. Certain items may not be liable for VAT, whereas the tax rate for other goods may be reduced. Furthermore, there may be certain supplies that are completely exempt from VAT and therefore not liable to VAT at all.

In general, a taxable supply is an important concept in the realm of Value Added Tax (VAT) and it significantly influences the tax responsibilities of both businesses and individuals. By having knowledge of what falls under the category of a taxable supply and how it is handled according to the law, companies can make sure they adhere to their tax responsibilities and evade any potential penalties or punishments.

EXEMPT SUPPLY

Exempt supplies pertain to items or services that are not liable to value-added tax (VAT) as they do not fall within the framework of VAT regulations. This indicates that there is no Value Added Tax (VAT) applied to these supplies, and businesses are not able to recover any tax paid on expenses associated with them. Exempt supplies are different from zero-rated supplies because they are also not charged with VAT. However, zero-rated supplies allow businesses to reclaim any input tax paid. This essay delves deeper into the notion of exempt supplies, investigating the reasons behind their exemption, the various types of supplies that fall under this category, and the consequences for businesses.

Exempt supplies play a crucial role in VAT regulations and can have substantial consequences for businesses engaged in supplying goods or services that qualify for exemption. Businesses must have a firm grasp of the regulations regarding exempt supplies in order to comply with VAT laws and effectively handle their tax obligations. This essay will delve deeper into the idea of exempt supplies, examining the rationale behind their exemption, the different types of supplies that are considered exempt, and the consequences for businesses.

One of the main purposes of excluding specific goods or services from being subject to VAT is to prevent instances of being taxed twice. In certain situations, products or services may have already undergone other indirect taxes prior to being purchased by the end consumer. For instance, insurance premiums may already face insurance premium tax, and adding VAT on top of it could lead to double taxation. Excluding specific supplies from VAT assists in guaranteeing that both businesses and consumers are not subjected to unfair multiple taxation on a single transaction.

Another purpose of excluding certain goods and services from VAT is to fulfill a particular policy goal. For instance, there may be exceptions for certain products or services in order to foster the well-being of society, boost particular sectors, or endorse specific actions. To give an illustration, VAT is frequently waived for healthcare services in order to guarantee that all citizens have access to essential medical treatment, regardless of their financial capability. In the same manner, educational services usually do not have to pay VAT in order to encourage education accessibility and foster continuous learning.

There are various kinds of supplies that are exempt and often mentioned in the VAT laws of many countries. These encompass a range of services such as financial, healthcare, education, and insurance services. Businesses must be aware of and follow the specific regulations in each category to avoid incurring penalties and interest charges related to VAT exemption.

Financial services, such as banking, insurance, and investment management, fall under the category of exempt supplies that are frequently provided. These services are not required to pay VAT because they are crucial for the economy and already subject to other taxes like bank levies or insurance premium tax. Excluding financial services from VAT is beneficial as it prevents double taxation on transactions for businesses and consumers while also preserving the competitiveness of financial markets.

Healthcare services, including but not limited to medical treatment, dental care, and nursing care, are classified as exempt supplies. These services are not subject to VAT as they are deemed necessary for preserving the overall health and welfare of the public. Excluding healthcare services from VAT assists in guaranteeing universal access to essential medical treatment, irrespective of one’s financial capability, and aids in strengthening the healthcare industry to provide top-notch care to patients.

Education services are frequently not subject to VAT in numerous countries. This group consists of offerings like fees for attending school, educational training sessions, and learning resources. Education services are not subject to VAT in order to encourage people to have access to education and to endorse continuous learning throughout their lives. Excluding education services from VAT is crucial to ensure equal access to excellent education for every individual, irrespective of their financial situation, and enhance upward social mobility and economic progress.

Insurance services, like property insurance, life insurance, and health insurance, are considered significant exempt supplies. These services are not subject to VAT as they are frequently taxed in other ways, like insurance premium tax, and are deemed essential for risk management and safeguarding individuals and businesses against monetary damages. Exempting insurance services from VAT assists in guaranteeing that businesses and individuals have access to cost-effective insurance coverage and contributes to fostering stability and security in society.

Furthermore, aside from the aforementioned general categories of exempt supplies, there exist particular regulations for additional kinds of supplies that might qualify for VAT exemption in specific situations. To illustrate, land and buildings may be excluded from VAT if they satisfy specific conditions, such as being utilized for residential objectives or charitable undertakings. In certain situations, the cultural sector may be exempted from paying VAT on cultural services, like museum admissions or theater tickets, in order to promote access to the arts and support this sector. Companies that provide goods or services that are exempt from VAT face various difficulties and repercussions when it comes to handling their tax responsibilities and ensuring compliance.

One of the main difficulties faced by businesses is figuring out the appropriate value-added tax (VAT) classification for their goods and services, as well as ensuring that they correctly adhere to the rules for exempt supplies. This can be especially challenging for businesses that provide a combination of items or services that are either exempt from or subject to taxes, as they need to meticulously monitor and document their sales in order to abide by VAT laws.

Managing the recovery of input tax is another obstacle that businesses face when supplying goods or services that are exempt. Businesses that provide goods or services that are exempted cannot recover any input tax associated with those supplies, unlike supplies that have zero-rated tax. Businesses must accurately assign their input tax expenses to taxable and non-taxable supplies to avoid either over or under-recovering input tax. If input tax recovery is not effectively managed, tax authorities may impose financial penalties and interest charges.

Companies that provide goods or services that are not subject to taxes also encounter difficulties in handling and setting their cash flow and pricing tactics. Businesses that provide goods or services that are exempt from tax may have to deal with increased expenses and reduced profit margins compared to businesses that offer taxable goods or services. This can pose challenges for businesses to effectively compete in the market and may necessitate them to modify their pricing strategies in response to the way VAT is applied to their products or services. Businesses should also take into account how exempt supplies can affect their cash flow. This is because they may have to pay VAT on their purchases without being able to recover it on their sales.

To sum up, exempt supplies have a crucial role in VAT regulations and can have significant consequences for businesses that provide exempt goods or services. It is essential for businesses to have a complete understanding of the regulations regarding exempt supplies. This knowledge allows them to comply with VAT regulations and effectively handle their tax responsibilities. Businesses can effectively comply with VAT regulations by diligently monitoring and documenting their sales, optimizing their input tax recovery, and adaptively strategizing their pricing methods while dealing with exempt supplies.

ZERO RATED SUPPLY

Zero-rated supply refers to a particular kind of provision where goods or services are not subject to the imposition of value-added tax (VAT). To put it differently, there is no Value Added Tax applied to these goods or services. This could bring advantages to both the supplier and the customer, as it has the potential to lower expenses and increase the affordability of certain products and services.

In this discussion, we will provide a detailed explanation of zero-rated supply. This will include an exploration of its definition, the requirements to be eligible for zero rating, and the consequences it has for both businesses and consumers. We will additionally examine instances of supplies with zero-rated taxation and assess the potential benefits and drawbacks of zero rating.

MEANING OF THE TERM “ZERO-RATED SUPPLY”

Zero-rated supply refers to the transaction of goods or services that are not subject to value-added tax (VAT). This implies that there is no value-added tax applied to these supplies, however, the supplier is still able to recover any VAT expenses incurred during the manufacturing or provision of the goods or services. Zero-rated supplies and exempt supplies are distinct as zero-rated supplies still incur VAT, but at a rate of 0%, allowing the supplier to reclaim input VAT, whereas exempt supplies involve no VAT charges and the supplier cannot reclaim any input VAT.

Zero-rated supplies are usually products and services that are deemed necessary or advantageous to society. These can consist of essential food items, healthcare services, and specific financial services. The aim of zero-rated supplies is to increase affordability and accessibility of these goods and services for consumers.

Zero-rating is a method of exempting certain goods or services from taxes or charges. It is a set of standards used to determine which items qualify for this exemption. For a supply to be eligible for zero rating, it must fulfill specific requirements outlined by the tax authority. The specific requirements may differ from one country or jurisdiction to another, but usually encompass the following:

1. The goods or services must be specifically listed as zero-rated in the VAT legislation. This means that not all goods and services are eligible for zero rating – only those that are deemed essential or beneficial to society.

2. The supplier must be registered for VAT and comply with all relevant VAT regulations. This includes keeping accurate records and submitting VAT returns on time.

3. The supply must be made to a customer who is also eligible for zero rating. This may include individuals, businesses, or other entities that meet certain criteria, such as being a charity or a not-for-profit organization.

4. The goods or services must be consumed or used in a certain way in order to qualify for zero rating. For example, certain medical supplies may only be zero-rated if they are used for the treatment of a specific condition.

IMPLICATIONS OF ZERO-RATED SUPPLY

The concept of zero-rated supply can have various consequences for both businesses and consumers. Zero-rated supplies can offer businesses a competitive edge as they allow them to reduce the prices of their goods or services, thus making them more economically accessible to customers. This has the potential to draw in additional customers and boost sales. Furthermore, companies that provide goods or services that are zero-rated might have the opportunity to recover any input VAT they have paid during the manufacturing or delivery process. This can ultimately result in cost reductions for the businesses.

Zero-rated supplies can provide consumers with the opportunity to purchase essential goods and services at a reduced cost, thereby making them more accessible and affordable. This can assist individuals and families with lower incomes in being able to afford essential needs like food, healthcare, and education. Zero-rated supplies can contribute to lowering the total expenses incurred by consumers, thereby positively affecting their standard of living.

Examples of Zero-rated Supplies

There are several examples of goods and services that are commonly zero-rated. These may include:

1. Basic food items such as bread, milk, and vegetables 2. Prescription drugs and medical supplies 3. Education services, including tuition fees and textbooks 4. Public transportation services 5. Financial services such as insurance and mortgage services 6. Exported goods and services

These are just a few examples of zero-rated supplies, and the specific goods and services that qualify for zero rating may vary depending on the country or jurisdiction.

Advantages and Disadvantages of Zero Rating

There are pros and cons to zero-rated supply. Some of the benefits are:

Affordability – Zero-rated supplies can help reduce the cost of necessary products and services for individuals, particularly those with limited financial resources.

Competitive advantage – Companies that provide goods or services without charging any taxes may gain a competitive edge compared to their counterparts who do charge taxes, as they have the ability to attract a larger customer base and boost their sales.

Cost saving – Zero-rated supplies enable businesses to lower their expenses by permitting them to recover the input VAT they accumulated during the production or delivery of goods and services.

However, there are also drawbacks to zero rating, which include:

Complexity – Identifying the goods and services that are eligible for zero rating can be challenging and time-consuming for businesses, particularly those that have a diverse range of offerings.

Revenue Loss – Zero-rated supplies have the potential to cause a reduction in government revenue as they do not incur any value-added tax charges. This can have an effect on the allocation of government funds for important services like healthcare and education.

Compliance Risk – Companies that provide products or services at a zero-rated VAT rate must adhere to all applicable VAT rules, which can be difficult and require a significant amount of time. Penalties and fines may be imposed for failure to comply.

In general, the exemption of taxes on certain products or services can have both beneficial and detrimental effects on businesses and consumers. Businesses should carefully evaluate the conditions for zero rating and guarantee adherence to all applicable VAT policies. Consumers have the advantage of enjoying cost-effective zero-rated supplies, however, they should also keep in mind any possible limitations or restrictions associated with these supplies.

To summarize, zero-rated supply pertains to the selling of goods or services that are not subject to VAT. These resources can have advantages for both companies and consumers, making necessary products and services more reasonably priced and easier to obtain. On the other hand, there are possible obstacles and dangers linked to zero rating, which encompass issues with obeying regulations and financial drawbacks for the government. In order to make well-informed decisions and comply with relevant regulations, it is crucial for both businesses and consumers to grasp the standards for zero rating and the consequences of zero-rated supplies.

Performance appraisal is the process of measuring quantitatively and qualitatively an employee’s past or present performance against the background of his expected role performance, the background of his work environment and his future potential for an organization. Evaluation of performance and personality of each employee is done by his/her immediate superior or some other person trained in the techniques of merit rating.

According to Edward Flippo “Performance Appraisal is the systematic, periodic and impartial rating of an employees’ excellence in matters pertaining to his present job and his potential for a better job”.

Performance appraisal is a broader term than merit rating, even though these two terms are used symmetrically. In merit rating, the focus is on judging the caliber of an employee so as to decide salary increment, whereas performance appraisal focuses on the performance and future potential of the employee. Merit rating measures the traits of the individual and performance appraisal measures the performance of the individual.

SIGNIFICANCE OF PERFORMANCE APPRAISAL

A performance appraisal provides a document of employees’ performance (Appraisal Forms) over a specific period of time.

A performance appraisal provides a structure where managers can meet and discuss performance with an employee.

A performance appraisal provides a structured process for an employee to discuss issues with their managers.

A performance appraisal can motivate employees if supported by a good merit and compensation system.

A performance appraisal is a systematic process consisting of a number of steps to be followed for evaluating the strengths and weaknesses of an employee.

PROCESS OF PERFORMANCE APPRAISAL

Establishing performance standards:

The employees will have to be rated against the standards set for their performance. There should be some base on which one may say that the performance of a person is good, average or even bad. The standards may be in quantity and quality of production. For eg: In case of workers-personality traits like leadership, initiative, imagination in case of executives; and Files cleared in case of office staff. These standards help in setting standards for evaluation of performance of employees.

Communicating standards and Expectations:

The standards set for performance should be communicated to the employees. They should know what is expected from them. Due to lack of knowledge of standards, the employees will keep on guessing. When standards are made know to employees they will try to contribute performance equivalent or above the standards. Even later on they will not resent adverse reports if they fail to achieve certain standards. It is essential to get feedback from employees whether they have followed the standards as intended by the management.

Measuring the actual performance:

The next step in evaluation process is to measure actual performance of employees. The performance may be measured through personal observation, statistical reports, oral reports and written reports.

Comparing Actual performance with Standards:

The actual performance is compared to the standards set earlier for finding out the standing of employees. The employee is evaluated and judged by his potential for growth and advancement. Deviations in performance are also noted at this stage.

Discussing Results with Employees:

The Assessment reports are periodically discussed with concerned employees. The weak, good points and difficulties are indicated for helping employees improve their performance. The information received by employees influences their performance, attitude and work in future.

Decision Making/Taking Corrective measures:

Evaluation process will be useful only when corrective action is taken on the basis of the report. One corrective action may be in form of advice, counsel or even as a warning. Other actions may be in form of additional training, refresher courses, delegation of more authority, special assignments, coaching etc.., These actions will be useful in helping employees to improve their performance in future.

OBJECTIVES OF PERFORMANCE APPRAISAL

1. Work- Related Objectives:

To assess the work of employees in relation to job requirements.

To improve efficiency

To carry out job evaluation

To help management in fixing employees according to their capacity, interest, aptitude and qualifications, i.e.., to ensure a right man is placed on the right job.

Career Development Objectives:

Career developments by means of formal and informal means the performance appraisal have the objectives to raise the opportunities for career development. On the basis of the results of appraisal, different system and programmes might be introduced for career development, orientation task and training programmes. A few objectives are as below:-

To determine career potential.

To assess the strong and weak points in the working of the employees and finding remedies for weak points through training.

To plan promotions, transfers, layoff and career goals of employees.

Communication:

Performance appraisal provides feedback to their employees about their performance and how they are working, how their efforts are contributing to fulfillment of Organizational objectives. Better performance is achieved when the employees are informed about their past performance and necessary corrective steps are taken to overcome deficiencies. A few objectives of communication of feedback with employees are as below:-

To clearly establish goals- what is expected of the employee in terms of performance and future work assignments.

To provide feedback to employees so that they come to know where they stand and can improve their job performances.

To develop positive superior-subordinate relations and thereby reduce grievances.

To provide coaching, counseling, career planning and motivation to employees.

Organizational Objectives: To serve as a basic of promotion or demotion. To serve as a basis for transfer or termination in case of reduction in staff strength.To serve as a basis for wage and salary administration and considering pay increases and increments.To serve as basis for planning suitable training and development programmes.

METHODS OF PERFORMANCE APPRAISAL

Strauss and Sayles have categorized appraisal method into two- Traditional Method and Modern method. While traditional method lays emphasis on rating of an individuals’ personality traits like intelligence, creativity, initiative, dependability, integrity etc.., On the other hand Modern method place more emphasis on evaluation of job achievements. They tend to be more objective and worthwhile. Performance appraisal is categorized as follows:-

TRADITIONAL METHOD

Essay appraisal method: Essay appraisal is one of the simplest methods among various other methods. In this method, the rater writes a narrative description on an employee’s strengths, weaknesses, past performance and suggestions for improvement. Essay method is simple and does not require complex formats and specific training to complete it. However, like other methods, its liberty less from drawbacks. In the absence of a prescribed structure, essays are like to vary widely in terms of length and content. The quality of appraisal depends on the rater’s writing skill than the appraiser’s actual level of performance. Since essay method is descriptive it only provides qualitative information about the employee. Evaluation suffers from subjectivity due to mitching of quantitative data. Nevertheless, the essay method is a good start and is beneficial also if used in association with other appraisal methods.

Paired comparison: In this method, each employee is compared to other employees on one-to-one basis, usually based on one trait only. The rater is provided with a bunch of slips each denoting pair of names. The rater puts a tick mark against the employee whom he thinks is better among them based on the quantity and quality of special knowledge about the inner workings of an organization / whom he insider the most among the two. The number of time this employee is compared as better with others determines his or her final rankings. The no. of. possible pairs for a given number of employees is ascertained from the following formula: N(N-1) 2

Where, N is the total number of employees to be evaluated.

Let’s have a look at an example. If 5 teachers are to be evaluated by the V.C of a University namely A, B, C, D, E. Substituting in the above formula the number of possible pairs would be 5*(5-1)/2 that will be 10 pairs. Below are the 10 pairs:-

A with B , A with C , A with D , A with E, B with C, B with D, B with E, C with D, C with E and D with E.

Straight ranking method: It is the simplest and oldest formal systematic method of performance appraisal in which employee is compared with all others for the purpose of placing order of worth. The employees are ranked from the highest/best to the lowest/worst. By doing this the employee who is in the highest on the characteristics and that on the lowest are indicated. If there are 10 employees to be appraised, there will be 10 ranks from 1 to 10. However, this method will not tell us how much better or worse one is than the other. The task of ranking individual is tougher when large numbers of employees are rated. It is difficult to compare one individual with others having varying behavioral traits. To antidote these defects paired comparison method of appraisal has been evolved.

Critical Incident method: In this method the rater focuses his or her attention on those critical behaviors that makes the difference between performing the job effectively or ineffectively. There are three steps involved in appraising employees using this method. Firstly, a list of remarkable on-the-job behavior of specific incidents is prepared. Secondly, A group of experts assign weights to these incidents depending upon their degree of desirability to perform a job. Thirdly, a final checklist indicating incidents that describe workers as good/bad is forged. Then the checklist is given to the rater for evaluating the workers. The basic concept behind this rating is to intimate the workers who can perform their jobs effectively in critical situations because most people work alike in normal situation. The strength of critical incident method is that it focuses on behavior and judges the performance rather than the personality. However, its drawback is that critical incidents are to be regularly written down which is time consuming and onerous for evaluators. Well, generally negative incidents are positive ones. It is the raters’ presumption that determines which incidents are critical and which are not to the job performance.

Check-list method The basicpurpose of using check-list method is to ease the evaluation burden on the rater. In this method a series of questions with their answers in “YES” or “NO” are prepared by the HR Department. The check-list is then presented to the rater to tick appropriate answers relevant to the appraisee. Each question carries a degree in relationship to their importance. When the check-list is completed it is sent to the HR department to prepare the final scores for all appraises based on all questions. While preparing the questions an attempt is made to measure the degree of consistency.

MODERN METHOD

Assessment centre : Assessment centre is not just a building for assessing a job candidate but instead it’s a process of evaluating the behavior based on multiple evaluation including job related simulations and psychological tests. Job Simulations are used to evaluate candidates on behaviors relevant to the most critical aspects (or competencies) of the job. Several trained observers and techniques are used. Judgments about behavior are made and recorded. These judgments are pooled in a meeting among the assessors or by an averaging process. In discussion among assessors, comprehensive accounts of behavior, often including ratings, are pooled. The discussion results in evaluations of the performance of the assessee on the dimensions or other variables.

During the assessment process, a set of exercises are designed to simulate the conditions of a work given to the candidate. This helps the assessor to determine whether the candidate possesses the necessary skill set and behavior required for the job. The sole purposes of assessment center are to examine the skills and psychological state of a person in order to determine his or her performance.

BARS ( Behaviorally Anchored Rating Scale)

Behaviorally Anchored Rating Scale is an appraisal method that aims to combine the advantages of narratives, critical incidents and quantified ratings by harbouring a quantified scale with specific narrative examples of good, medium and poor performances.

360° performance appraisal.

The 360 degree feedback is an appraisal tool that incorporates feedback from all those who observe and are affected by the performance of a candidate. The feedback received from 360° performance appraisal is generally used to plan training and development.

ETHICAL ISSUES IN PERFORMANCE APPRAISAL

Performance appraisal is used as the basis of so many HR decision s like promotions, dismissals and transfers. The appraisal system is a common target of legal disputes by employees involving charges of unfairness and personal biases. Generally, employees seek legal help to obtain relief from a discriminatory performance appraisal. Unreasonably rating everyone high/low on the basis of past events are some of the reasons judiciary give for deciding the organizational appraisal processes. Most employees find that the appraisers can stick to the rules and do lawful performance appraisal reviews yet they fail to provide honest assessments. Over the years several recommendations have been made to assist the employers to develop fair and legally defensible performance appraisal system. Some of which are as below:-

Every organization should have a formal standardized performance appraisal system. All the HR decisions should be based on this system.

There should be uniformity in the application of performance appraisal process for all the employees within a job group. The decisions based on these performance appraisals can be monitored for differences in caste, religion or age of the employee.

All employees should be given opportunities to review their appraisal results.

All employees should be aware of all specific performance standards.

There must be a formal appeal process where an employee can question the rating given by the appraiser.

All HR decision makers should be well informed about the anti-discrimination laws.

Supervisors (Appraisers) should be trained to use the appraisal tools properly. If formal training is not possible then written instructions should be provided to all raters for using rating scales in an unbiased and systematic manner.

BENEFITS OF PERFORMANCE APPRAISAL

(Source : eduCBA.com)

The benefits that justify the existence of a system of performance appraisal in an organization are as follows:

Performance appraisal provides the management an objective basis for discussing salary increase and special increments of the staff.

A performance appraisal can be used for transfer or promotion of employees. If the performance of an employee is better than the others, he can be recommended for promotion. But if he is not doing well then, he may be transferred to some other job for which he is best suited.

An effective system of performance appraisal helps the supervisor to evaluate the performance of his employees periodically and systematically. It helps in placement of employees on the jobs for which they are best suited for.

Performance appraisal facilitates Human resource planning, career planning and succession planning.

It provides an incentive to the employees to improve their performance in a bid to better their rating over others.

Work environment improves when achievements are recognized and rewarded on the basis of objective performance measure.

A Systematic appraisal of performance helps to develop confidence among employees. It will prevent grievances, if the employees are convinced of the impartial basis of evaluation.

Thus, Performance appraisal is a significant element of information and control system in an organization. Performance appraisal can be put to several uses concerning the entire spectrum of Human Resource Management function.

The HR managers usually make errors in performance appraisal process. Let’s have a look at those errors. One such error is Rater Error. As you all know the famous saying by Alexander Pope- “To err is human”, it is common for managers to make subconscious errors when assessing employee behavior and preparing a performance appraisal document. These rater errors are pensive of our subconscious biases towards the employee and these biases can give an employee an unfair advantage or disadvantage over others in their peer group. It is important to understand these biases and anticipate while preparing a performance appraisal document.

WHAT ARE RATER ERRORS? There are six common errors we make while assessing the performance of others. Being conscious about these errors can help the HR to avoid errors.

Halo Effect: This occurs when a rater’s overall positive or negative impression of an individual employee leads to rating him/her the same across all rating dimensions. This happens when a manager really likes or dislikes an employee and allows their personal feelings about this employee to influence their performance rating on them. Let’s think of that favorite employee you might be comfortable with or that employee with whom you have a personal rivalry with, and ask one-self that- Am I being objective with this assessment?

Never

Sometimes

Always

1

2

3

4

1

2

3

4

1

2

3

4

1

2

3

4

1

2

3

4

Leniency error: This error happens when a raters’ tendency is to rate all employees at the positive end of the scale (positive leniency) or at the negative end of the scale (negative leniency). Sometimes, our emotions determine how we rate an employee and this response might not be objective since it is emotional in nature. This usually happens when a manager over emphasizes either positive or negative behaviors.

Never

Sometimes

Always

2

3

4

2

3

4

2

3

4

2

3

4

2

3

4

Central tendency error: This error is the rater’s tendency to avoid making “extreme” judgments of employee performance resulting in rating of all employees in middle section of a scale. This happens either when a manager is not comfortable with conflict and avoids low ratings to avoid dealing with behavioral issue or when a manager forces all employees to the middle of the scale.

Never

Sometimes

Always

1

2

4

5

1

2

4

5

1

2

4

5

1

2

4

5

1

2

4

5

Recency error: This error is the rater’s tendency to allow more recent effective or ineffective incidents of employee behavior to carry too much weight in the performance evaluation over an entire rating period. Either an employee completes a major project or an employee may have encountered a negative incident before the performance appraisal process and it is at the cutting edge/front line of the manager’s thoughts about the employee. For this reason it is important to keep accurate records of performance throughout the entire year to refer back to during performance appraisal.

First Impression Error: This error is the rater’s tendency to let their first impression of an employee’s performance to carry too much weight in the evaluation process over an entire rating period. For e.g. A new employee joins the organization and performing at high levels during their “honeymoon” period and possibly losing some of that initial momentum.

Similar-to-me Error:

This error happens when the rater’s tendency is biased in performance evaluation towards those employees seen as similar to the raters themselves. We can relate to people who are like us but we cannot let our ability to relate with an individual influence the parameters on which their performance is judged in a professional working environment. Since human biases can easily influence the rating process it is important to create objective measures for rating performance. Observing behaviors and using available technology to track performance can eliminate some of the biases from the rating process.

CONCLUSION

Performance appraisal is very important as it affects the productivity of employees’, their relation with superiors and subordinates which in turn increases the morale of the employees’. Awareness must be spread among employees so that they get to know the importance of performance appraisal. It is generally found that personal bias creeps in appraising an individual. An Organization must implement latest techniques of performance appraisal so as to yield better results by improving productivity of the employees since confidence development is the main focus of performance appraisal. The technique used and what is expected from the employees must be stated clearly.

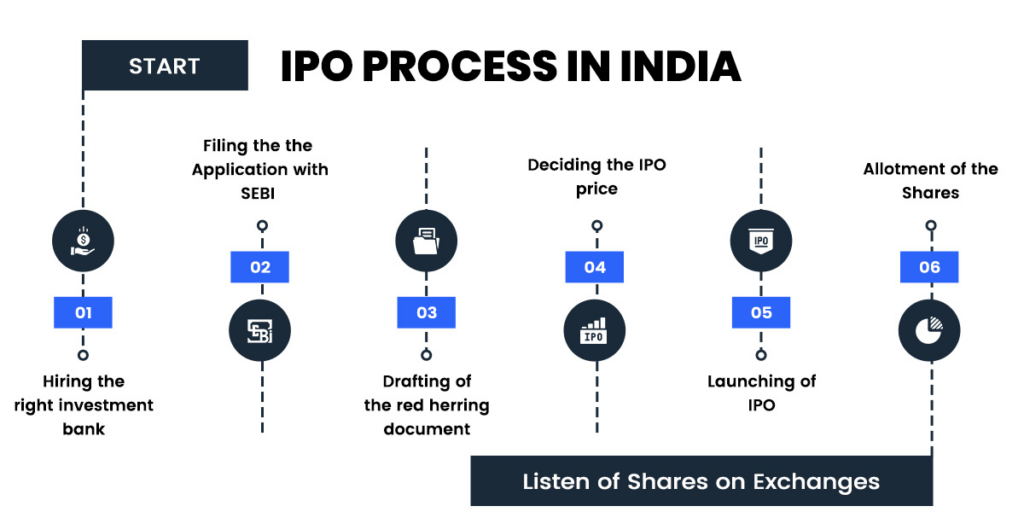

An IPO or Initial Public Offering, is the process by which a privately held company offers its shares to the public for the first time. Typically, it is done through a stock exchange, such as the New York Stock Exchange, NASDAQ (National Association of Securities Dealers Automated Quotations), NSE (National Stock Exchange), BSE (Bombay Stock Exchange), OTC (Over-the Counter) exchange of India.

The listing process generally involves several steps, including preparation of an offering prospectus, selection of investment bank to underwrite the offering, determination of offer price, and completion of regulatory filings with the appropriate securities regulators. Once the IPO is completed and the shares are listed on a stock exchange, the company become subject to public reporting requirements and must comply with regulations governing public companies. An IPO listing can provide a company with access to capital to fund growth and expansion, increase its visibility and credibility in the market, and to provide liquidity to its existing investors. It can also offer employees and early investors an opportunity to realize gains on their equity holdings.

As mentioned before the, IPO process involves several key steps that requires careful planning and execution.

Hiring an underwriter: The initial phase of getting ready for an IPO involves enlisting the services of an underwriter, usually an investment bank, to assist in the process of making the offering. The underwriter will assist the company in deciding the price, schedule, and magnitude of the initial public offering (IPO).

Conduct due Diligence: The company must go through a comprehensive due diligence procedure to verify that all financial and legal aspects of the business are arranged properly. This will require a thorough examination of financial statements, legal papers, and other essential data.

Prepare a prospectus: The company will have to get ready a prospectus, which is an in-depth document that gives comprehensive information about the company and the opportunity to potential investors. The prospectus will provide details regarding the company’s business model, its financial performance, any potential risks, and other significant information.

Register with the Securities and Exchange Commission (SEC):The company must complete the registration process with the Securities and Exchange Commission (SEC) and submit all necessary paperwork, such as the prospectus, before proceeding with the IPO.

Market the offering: The company and its underwriters will collaborate to generate enthusiasm for the IPO through roadshows and meetings with prospective investors. This will aid in creating interest for the product/service and deciding on the ultimate price for it.

Price the offering:After assessing the level of demand, the company and its underwriters will establish the ultimate selling price for the offering. This will determine the amount of funds the company will generate via the initial public offering (IPO).

Go Public:On the scheduled day of the Initial Public Offering (IPO), the company will make its official debut in the stock market by offering shares to the general public for their first-time purchase. The stocks of the company will be available for trading on a stock exchange, allowing investors to purchase and sell them.

Post IPO activities:Following the initial public offering, the company will be required to uphold regulatory obligations, sustain public documentation, and engage in regular communication with investors. The company must also actively monitor and control its stock price to meet investor expectations.

Overall, preparing for and executing an IPO is a complex and time-consuming process that requires careful planning and coordination. However, a successful IPO can provide a company with access to the public markets and a significant infusion of capital to help fuel growth and expansion.

Benefits and Risks of IPO associated with going Public

An IPO can provide a number of benefits to both the company and its investors. Let’s discuss some benefits of Initial Public Offer (IPO) to the Public.

Capital raising: When a company goes public via an IPO, it can generate substantial funds by offering shares to the general public. These funds can be utilized for different objectives like growing the business, conducting research and development activities, or paying off debts.

Increased Liquidity: By being listed on the stock market, individuals can easily purchase and sell shares through a public exchange, allowing them to quickly convert their investments into cash.

Enhanced visibility and credibility: Becoming publicly traded can enhance a company’s presence and reputation in the market, enticing customers, collaborators, and prospective investors.

Employee incentivization: Publicly traded corporations have the ability to provide employees with stock options and other forms of compensation tied to the value of the company, which can be advantageous in enticing and keeping highly skilled individuals.

Acquisition currency: Publicly traded corporations often have a greater market value, which they can utilize to procure other businesses or resources by means of stock-related deals.

Risks of IPOs

Purchasing shares in an IPO can provide an exhilarating chance to acquire ownership in a recently listed company. Nevertheless, it has its own set of dangers. Initial public offerings (IPOs) can often experience significant fluctuations and are difficult to forecast, making it uncertain whether the stock price will rise after the company becomes publicly traded. Investors need to thoroughly assess the potential hazards prior to making a decision to invest in an initial public offering (IPO). IPOs come with certain risks which include uncertain market conditions, absence of past performance records, inadequate information, and the possibility of the company being overpriced. Few of the risks are discussed below.

Cost and complexity: Engaging in an initial public offering (IPO) can prove to be an expensive and intricate procedure, which involves considerable financial burdens related to legal, accounting, and underwriting charges.

Regulatory scrutiny: Publicly traded companies must adhere to more stringent regulations and reporting obligations, encompassing financial transparency and corporate management regulations, which can be inconvenient and time-consuming.

Share price volatility: Publicly listed corporations face the risk of market turbulences, and external factors like overall economic situation and investor perception can impact their stock prices.

Loss of control: When a company becomes publicly traded, it’s existing shareholders may experience a reduction in their ownership and control over the company. Additionally, they may face heightened scrutiny and pressure from the public shareholders and analysts.

Short-term focus: Publicly traded companies may experience demands to achieve immediate outcomes in order to appease shareholders, resulting in decisions that prioritize short-term gains over the long-term welfare of the company.

Preparing for an IPO

Introduction

An IPO is a significant event for a company as it marks the transition to being publicly traded. This includes the act of selling portions of the company to the general public for the very first time, allowing investors the chance to possess a share in the business. Before companies can go public, they need to go through a thorough process of financial and legal investigation, in addition to carefully planning their strategies. This is crucial to guarantee a seamless and prosperous transition to the public markets. Careful evaluation of market conditions, investor demand and regulatory requirements is necessary to optimize value for both the company and its shareholders in this procedure.

Assessing the company’s readiness for an IPO

IPO is a major achievement for any company. An initial public offering (IPO) refers to the act of a privately owned company introducing its shares to the public for the first time. This enables the company to raise funds and allows investors to purchase and trade shares in the company. However, an initial public offering (IPO) is an intricate and demanding procedure that necessitates meticulous planning, preparation, and evaluation of the company’s state of readiness to be publicly available for investments. The company needs to evaluate its financial condition, market standing, potential for growth, and operational abilities before taking into account the possibility of going public. This evaluation entails a comprehensive examination of the company’s business model, sources of income, ability to generate profit, liquidity, and practices related to financial management. In order to allure investors and facilitate a successful initial public offering, the company needs to possess a solid financial position, effective financial management systems, and a sustainable path of growth.

Besides thinking about financial factors, the company needs to assess its market position, competition, and the overall dynamics of the industry. To fully comprehend the worth of a company, it is crucial to conduct a thorough analysis of the market, which will provide insights into the company’s unique selling point, the audience it aims to cater to, the advantages it possesses over its competitors, and the potential for future expansion. To convince investors of its long-term potential, the company needs to present a convincing rationale for its business and demonstrate a clear plan for sustainable growth. Operational preparedness is another critical element that establishes the company’s level of preparedness for an initial public offering. In order for the company to grow and expand, it is essential to have a capable management team, a well-functioning governance structure, and operational systems in place. The company also needs to possess robust internal controls, risk management protocols, and compliance procedures in order to fulfill the regulatory obligations of being a public company.

Apart from these internal factors, the company must also evaluate external market situations, investor attitude, and regulatory circumstances to decide the best moment for an initial public offering (IPO). The success of an IPO can be influenced by market volatility, economic conditions, and industry trends. Therefore, the company needs to thoroughly assess these elements in order to increase its likelihood of success.

In summary, evaluating the company’s preparedness for an initial public offering is an essential stage in the process of becoming publicly traded. The company needs to assess its financial wellbeing, market status, potential for growth, and operational abilities extensively in order to gauge its readiness for an IPO. By thoroughly assessing these elements and rectifying any deficiencies or deficiencies in its preparedness, the company can enhance its prospects of a prosperous initial public offering and access fresh avenues for development and advancement.

Selection of underwriters and other advisors

When choosing underwriters and other advisors for an IPO, it is important for companies to thoroughly assess the skills, knowledge and past performance of potential candidates. When selecting underwriters and other advisors for an IPO, there are several important factors to take into account. They are:

Reputation and Experience: Look for underwriters and advisors with a strong reputation and track record of successfully executing IPOs in your industry or sector. Consider the volume and size of deals they have worked on, as well as their overall success rate.

Industry Expertise: Select underwriters and advisors with industry expertise and a comprehensive understanding of market dynamics that are specific to your business. This can assist in guaranteeing that they are able to efficiently promote your IPO to investors and optimize valuation.

Global Reach: It is important to look for underwriters and advisors who have a strong global reach and presence, particularly if you intend to appeal to international investors or list your company on multiple stock exchanges.

Relationship and Chemistry: Forming a strong professional bond with your underwriter and advisor is essential for a fruitful IPO procedure. Ensure that you schedule meetings with prospective candidates and evaluate their manner of communication, level of responsiveness, and compatibility with the culture of your organization.

Fee Structure and terms: Assess the proposed fee structure, costs, and terms from potential underwriters and advisors. Although cost should not be the sole consideration in making your decision, it is crucial to ensure that the charges are both are competitive and clearly stated.

Value added services: Think about the extra services and assistances that the underwriters and advisors can provide apart from the IPO procedure. This can include on-going support for investor relations, strategic guidance and opportunities to explore potential business ventures.

Due diligence: Complete a comprehensive investigation on potential underwriters and advisors, which involves examining their regulatory track record, identifying any conflicts of interest and assessing any previous legal or regulatory problems they may have had.

In the end, making the right decision about the underwriters and advisors for your IPO is crucial as it can greatly affect the success of your Initial public offering and the future performance of your company in the public market. Spend some time thoroughly assessing your choices and pick partners who can most effectively assist in achieving your IPO goals and objectives.

Conducting financial due diligence and preparing financial statements

Financial due diligence involves assessing a business’s financial performance, position, and risk to uncover any possible problems or warning signs that may affect an IPO. This includes the examination of financial documents like accounting records, financial statements, and tax returns, as well as conducting interviews with important management personnel and other people involved in the matter.

Financial analysts and accountants will review the company’s past financial performance during the due diligence process. This analysis will cover areas such as revenue, profitability, cash flow, and liquidity. They will also review the financial status of the company, including its assets, debts, and ownership, to verify the accuracy and dependability of the financial statements.

Furthermore, the process of conducting due diligence will involve evaluating the financial risks of the company, such as possible liabilities, potential future liabilities, and any financial responsibilities or commitments that may have an influence on the company’s overall financial well-being.

After finishing the financial due diligence, the company will create its financial statements in compliance with regulatory requirements and accounting standards. This usually includes the preparation of a balance sheet, income statement, and cash flow statement, along with any other necessary financial disclosures needed for an Initial Public Offering (IPO).

In general, performing financial due diligence and creating financial statements are vital procedures during the IPO process. These steps are essential in guaranteeing that investors are provided with precise and trustworthy financial data to enable them to make well-informed investment choices.

Developing a business plan for IPO

An IPO refers to the mechanism through which a privately owned company introduces its stock to the public for the first time by making shares available for purchase. Creating a comprehensive plan for a business’s initial public offering (IPO) is essential for attracting potential investors, ensuring a prosperous public offering, and clearly defining the company’s strategy for growth. These are essential elements to incorporate in a business plan for an Initial Public Offering (IPO):

Executive Summary:Summarize important information about the company, such as its background, offerings, target audience, advantages over competitors, notable financial achievements, and significant accomplishments.

Company Overview:Explain the organization’s operational strategy, the current state of the industry, competition, potential market size, and prospects for expansion. Identify the distinct value proposition that differentiates the company from its rivals.

Financial performance:Provide historical financial information, including figures for revenue, profitability, cash flow, and important performance indicators. Please provide future growth forecasts that highlight the methods in which the company intends to generate more revenue and broaden its market reach.

Management Team: Provide a comprehensive overview of the professional backgrounds and qualifications of essential executives and board members, highlighting their expertise in the industry, their skills in leadership, and their impressive history of accomplishments.